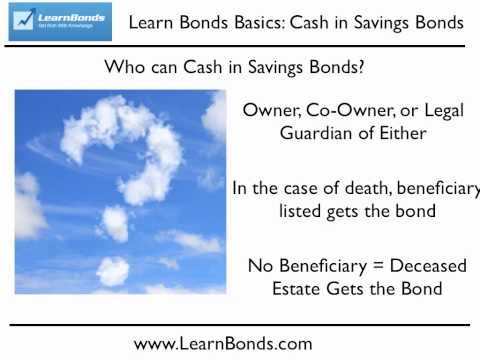

Hi folks, Dave Waring here again with Learn Bonds. Today we're going to talk about how to cash in savings bonds. You cannot cash in savings bonds that are less than one year old. After holding a savings bond for more than one year, you can cash it in at any time. However, there are some additional factors to consider. First, if you cash in your savings bond within the first five years of purchase, you will have to forego the previous three months' interest payments. Second, savings bonds fully mature in 30 years, meaning they stop earning interest at that point. Third, you can cash in a savings bond at any time after the 30-year maturity date, but you do not earn any additional interest when holding for longer than thirty years. In order to cash in a savings bond, you must be the owner, co-owner, or legal guardian of either the co-owner or the owner. You can also cash in a savings bond if you have power of attorney over the owner or the co-owner. If the owner of the bond has died, then the bond goes to the beneficiary listed when the bond was purchased. If there is no beneficiary listed, the bond goes to the estate of the deceased owner. The primary owner and co-owner listed have equal rights over the bond, meaning the co-owner can redeem the savings bond without the owner's consent, and vice-versa. With this in mind, be sure to take careful consideration over whom you list as your co-owner. There are two ways that you can cash in a savings bond. You can do it electronically through Treasury Direct or through a local participating bank. However, it's unclear how many banks will provide savings bond redemption services now that the government has stopped issuing...

Award-winning PDF software

8815 requirements Form: What You Should Know

A 100,000 bond will be included as earned interest if it matures in 2025 and will be redeemed either in 2025 or in 2020. The interest received on a Series I or EE bond must be reported on the return. Series I and F bonds that mature in 2025 will be included on Form 8949, Return of Investment Income and Expenses. Exclude your interest from income on a bond that matures before September 13, 2020: “You should exclude interest (earned from maturity) on Series I or III bonds from the income of the decedent whose estate you're paying.” This has no tax effect under current law. Exclude all interest from Series I, II, or III bonds from the decedent's income. This rule does not apply if the interest is received by the decedent before the death date. You can exclude the entire interest from your estate. Don't deduct interest expenses from the estate. Don't include interest on a debt other than Series I, III, or VIII bonds; Series IX bonds; or Series VIII bonds, but just as a basis for determining the amount of the payment. Form 8949 — Return of Investment Income and Expenses You can exclude the interest on all cash and cash equivalents to the extent you meet these following requirements: 1. You can deduct only the fair market value of the assets at the time of the payment. 2. The interest includes any principal, interest, or any other fee, premium, reward, dividend, equivalent, or additional compensation paid, or any fee, price supplement, or price alteration with respect to the property. 3. You can't have the entire interest excluded. Even partial exclusion is still taxable under current law. If you elect not to take the gross estate tax deduction for the interest, there's no estate tax paid on the interest. For more information on the tax you may pay on Series I and II savings bonds, see Publication 547.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8815, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8815 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8815 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8815 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Form 8815 requirements